If you’ve followed my writing for a while, you already know I bounce between three big themes: Creative Entrepreneurialism, Creativity & Creative Process, and Personal Finance.

The first two are crowd favorites. The last one? Not so much. But it’s the one I feel the deepest responsibility to write about—because I’ve lived what happens when you ignore it.

Entrepreneurs and creatives are wired for optimism. We assume the big break is coming. We assume we’ll figure out money later. We assume our success will catch up with our spending.

I used to believe all that too—until life introduced me to reality.

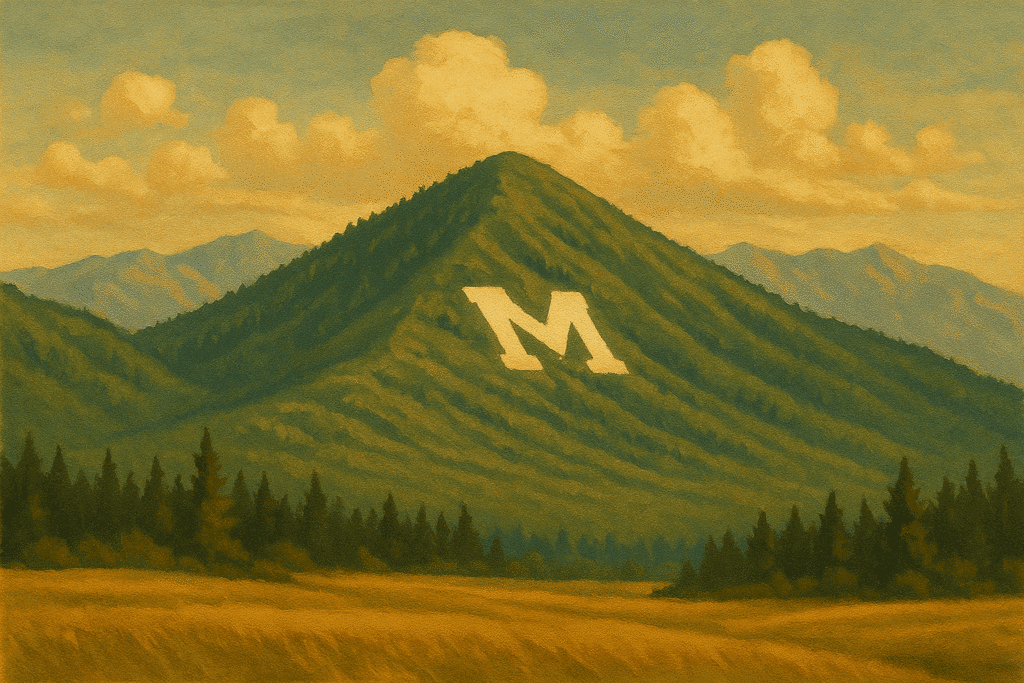

The Bozeman “M”: A Daily Reminder Out My Window

Since I live in Bozeman, let me start with a metaphor that’s literally in my line of sight every day. When I look up from my home office desk, I stare straight at the giant white “M” carved into the side of Mount Baldy. It’s bright, bold, and impossible to ignore—a permanent reminder about the cost of steep climbs.

If you’ve hiked the M, you know there are two trails:

1. A long, gradual set of switchbacks.

2. A brutally direct ascent straight up the mountain.

Watch the foot traffic and you’ll notice something:

Younger hikers charge up the steep route. Older hikers take the switchbacks.

Not because they lack courage—but because steep climbs get harder with age.

Money works exactly the same way.

Get into credit-card debt or wait too long to start saving for retirement, and you’ve effectively chosen the straight-up path.

No switchbacks. No pacing. Just pain.

That “M” isn’t just a landmark to me—it’s a motivator. It reminds me why I teach this stuff: to help people choose the easier trail before life forces them onto the hard one.

When It Rains, It Pours (My $135,000 Mistake)

People assume financial advisors live perfectly disciplined financial lives.

Not me.

I was 40 when I finally got my financial house in order.

In 2007, I took on a major home addition in Maine. We burned through the construction loan before the house was done, and—like a lot of overwhelmed families—we turned to credit cards to finish the job.

Then came the 2008 crash.

- Real estate collapsed.

- Stocks collapsed.

And when I did my first true Net Worth Statement, I discovered:

I was $135,000 underwater.

That was my steep trail. And there were no switchbacks available.

Building Our Way Out—One Long Night at a Time

My wife (@Wild_Woman_MT) and I did the only thing we could: we went to work.

We were running her online business at the time—back in the era when building an online store meant rolling up your sleeves and learning code. There were no drag-and-drop builders. No AI tools. No Shopify themes. You had to know HTML, CSS, image optimization, FTP uploads, metadata, SEO, key wording and how to debug things manually. We scaled fast because we had to.

Those nights were brutal.

Babies sleeping on the floor next to us while we packed boxes until 2 AM. Stacks of orders filling the living room.

Multiple trips to the post office, where the staff eventually let us load directly into the canvas bins in the back because we showed up with so many packages every day.

Every spare dollar—every single one—went against those credit card balances.

Interest rates climbed as high as 35%. When you’re on the robes is just when the vampires really comes in.

It felt like climbing the steep side of the “M” in the snow, carrying a refrigerator.

But step by step, dollar by dollar, we climbed out.

I DIY’d My First Personal Financial Plan

Funny thing: I started my career at Morgan Stanley. They didn’t teach us how to build financial plans. They taught us how to sell products.

So I had to teach myself.

I listened to hours of Dave Ramsey, absorbing his core principles.

I didn’t always use his exact methods, but the principles changed my life—and became the foundation of the first financial plan I ever built: my own.

That experience eventually led me to build real plans for clients. Because I had lived the pain—and transformation—personally.

Techniques Change. Principles Don’t.

There’s a line from The Art and Science of Digital Marketing that has always stayed with me:

“Techniques and methods may change, but principles remain the same.”

It’s true in digital marketing, where trends move at what I call the speed of light—literally, electrons flying across wires. Online business is endlessly competitive and constantly shifting.

I’ve built in that world for over two decades. I have the battle scars to prove it.

But personal finance?

- That world is slow.

- Stable.

- Timeless.

Dave Ramsey used physical envelopes. I created my Digital Envelope System.

Clients use spreadsheets, apps, automations, cash-only systems—you name it.

The technique doesn’t matter.

The principle does:

Spend less than you earn and stay consistent.

That principle saved my financial life. And I still apply it every single day.

How I Live It Today—Even With Two Homes

I now own two homes—one in Maine and one in Montana—but I still live by the principle.

Recently I booked a flight back to Montana after Christmas. The options were:

- $135 one-way ticket with two layovers and 11 hours travel time.

- $750 one-way ticket with one layover and about 8 hours travel time.

Easy choice.

For me and Kerry, that’s $1,230 in savings for just a few hours difference.

Don’t forget, I can work from airports. I can talk to clients and place trades. No problem. I set up my iPhone’s hotspot connect MacBook and I’m up and running.

I can also write, edit, or plan content on planes and I download movies on Netflix ahead of time instead of paying $20–$25 for in-flight Wi-Fi.

And don’t forget about old-fashioned books. That ties nicely back into one of my life principles – sharpening the saw.

Sage Advice: Establish a habit of lifetime learning. It’s how you develop your human potential and increase your human capital.

Human capital is another way of saying how much you can earn in the years you have left until you retire.

There are two inputs:

- The hours you have left to work in your lifetime.

- The value of your time.

Your time is finite. Only so many hours left in a day and in a lifetime. Unchangeable.

But what you earn for your hours. That is flexible. It can be increased with experience, knowledge, skills and entrepreneurship. If you’re so inclined.

Remember, we talked about this is Part 2.3: The Spending Plan.

Ways to reach your goals:

- Increase your income.

- Reduce your spending.

But I was talking about reducing your spending, so here are some things to think about:

- Frugality isn’t deprivation.

- It’s discipline.

- And discipline compounds.

Why I Teach This—and Why I’ll Keep Teaching It

Everything I share—this story, my tools, my mistakes, my systems—flows directly into my Financial Planning Made Simple series. I teach this stuff from two deep wells of lived experience:

- Online business at the speed of light

- Personal finance at the speed of compounding

Both matter. Both shape your future. Both can change your life.

My hope is simple:

- Start early.

- Take the switchbacks.

- Learn the basics.

- And build a plan before you need one.

I’ll walk you through every step.