If you’re a high-income solopreneur or small business owner with just a handful of employees, a traditional IRA OR ROTH IRA isn’t going to cut it if you want to save on taxes and maximize retirement savings. With contribution limits of just $7,000 per year (or $8,000 if you’re over 50), it’s barely a rounding error when you’re bringing in serious income.

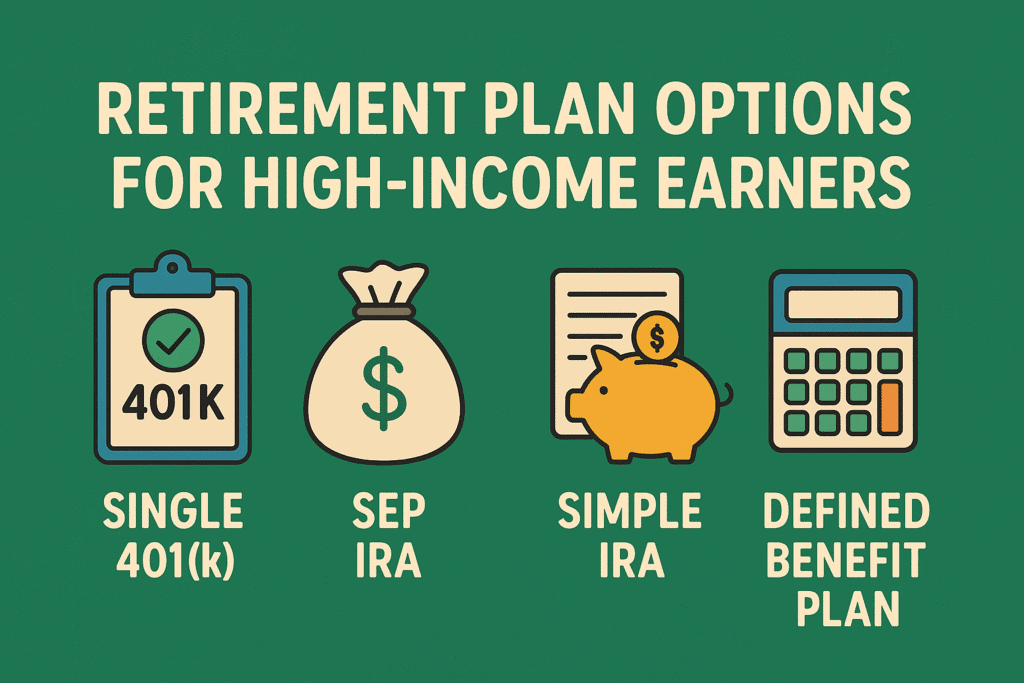

Below, we’ll break down the three main retirement plan options available to high income solopreneurs, entrepreneurs and small business owners:

- Solo 401(k)

- SEP IRA

- SIMPLE IRA

In Part 2, we’ll explore an advanced strategy most people don’t even know exists — the Defined Benefit Plan, which can allow you to contribute $200,000+ per year.

Solo 401(k): The Heavyweight for One-Person Businesses

The Solo 401(k) (also called an Individual 401(k)) is one of the most powerful tools available if you’re self-employed with no full-time employees — or only your spouse.

Key Features:

- Max Contribution (2025): Up to $70,000 — or $77,500 if you’re 50 or older

- Structure: You contribute both as the “employee” (deferral) and “employer” (profit-sharing)

- Roth Option: You can contribute after-tax dollars for tax-free growth

- Loan Option: You can borrow from it, just like a traditional 401(k)

This plan allows you to stack retirement savings fast. For example, if your net income is $150,000, you could:

- Contribute $23,500 as employee deferral (plus $7,500 catch-up if over 50)

- Add up to 25% of your compensation (up to $37,500) as the employer

Downside: The Solo 401(k) only works as long as you have no employees (except your spouse). As soon as you hire full-time help, the plan is no longer compliant. You’ll have to shut it down and transition to a traditional 401(k) or another plan that accommodates employees.

Still, for high-income solopreneurs, just starting our entrepreneurs or self-employed individuals like real estate agents, this is usually the first — and often the best — place to start.

SEP IRA: Big Contributions, But Less Control

The SEP IRA (Simplified Employee Pension) is a favorite among small business owners because it’s easy to set up and allows for large contributions but it comes with strings.

Key Features:

- Max Contribution (2025): Up to 25% of compensation, capped at $70,000 for 2025

- Employer Funded Only: No employee deferrals allowed

- No Roth Option

- Easy Setup: Minimal forms, low maintenance

The Big Catch: If you have employees, you must contribute the same percentage of their salary as you contribute to your own.

Example:

- You earn $200,000 and contribute 25% ($50,000) to your SEP IRA.

- You have one employee who earns $60,000.

- You must contribute 25% of their salary too — $15,000 — whether or not they ask for it.

This can get expensive fast as your team grows.

Another downside? Employees don’t need to contribute a dime. While that may sound generous, it can backfire. Many business owners prefer retirement plans that reward employees who participate, not just hand out money regardless of behavior.

SIMPLE IRA: Affordable and Familiar

If you have a few employees and want a plan that’s easy to manage and familiar to your team, the SIMPLE IRA is a solid option.

Key Features:

- Max Employee Contribution (2025): $16,500 (+$3,500 catch-up if 50+)

- Employer Match: Either:

-

- Dollar-for-dollar match up to 3% of salary (if the employee contributes), or

- 2% non-elective contribution to all employees.

- Low Admin Cost: Very easy to set up and maintain

Unlike the SEP IRA, employees must contribute in order to receive the match — if you choose the matching structure. That’s a big win for employers who want to incentivize smart financial behavior instead of just giving out retirement money to everyone, regardless of participation.

Limitation: The contribution limits are much lower than a Solo 401(k) or SEP IRA. If you’re earning $200K+ a year, you’ll likely outgrow a SIMPLE IRA pretty quickly.

Still, for a small business with moderate income and a couple of employees, it’s a low-friction, low-cost starting point.

How to Choose the Right Plan

Here’s a simple way to look at it based on your current situation:

Situation |

Likely Best Option |

|---|---|

| Solo business, no employees | Solo 401(k) |

| You want to max tax savings, don’t mind contributing for employees | SEP IRA |

| Small team, want low-cost setup and shared contributions | SIMPLE IRA |

| You’re earning 7 figures and want to shelter $200K+ | Defined Benefit Plan (coming in Part 2) |

Remember: the best plan isn’t just about the numbers — it’s about your strategy. Do you want flexibility? Do you want to incentivize employees to save? Do you want to aggressively reduce taxable income?

Coming Next: The $200K+ Strategy Most People Miss

If you’re consistently earning high six or seven figures, there’s one retirement strategy that’s rarely discussed: the Defined Benefit Plan.

It’s not for everyone — it’s complex, requires ongoing actuarial calculations, and must be funded consistently. But if you’re the right candidate, it can allow you to shelter $200,000 or more per year, pre-tax.

And it works even if you have employees — there are creative ways to structure it to maximize your benefit while managing costs.

Stay tuned for Part 2 — we’ll break it down in plain English.

Final Word: Turn Your Retirement Plan into a Wealth Engine

The right retirement plan can do more than just help you retire — it can shrink your tax bill, reward key employees, and build long-term wealth faster than most people realize.

Most high-income business owners wait too long to upgrade their plan — or never do. The earlier you act, the more you can leverage compound growth and tax advantages.