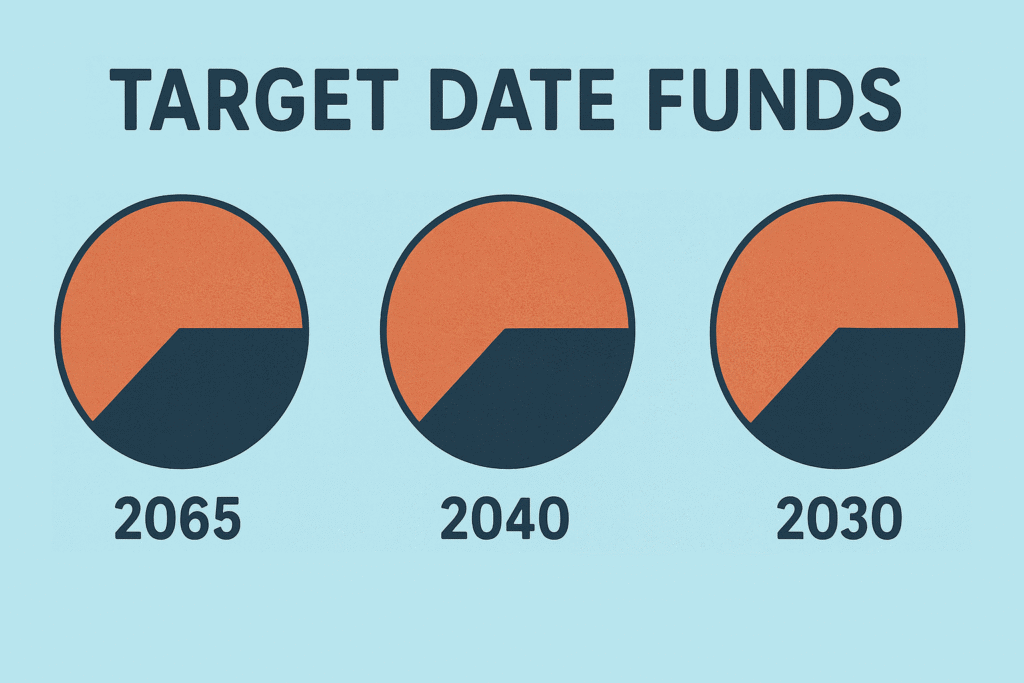

What Is a Target Date Fund?

A target date fund (TDF) is a type of mutual fund or ETF designed to simplify retirement investing. You pick the fund that matches your expected retirement year—like a Target Date 2050 Fund—and the fund takes care of the rest. It automatically adjusts its mix of stocks and bonds over time so that your investments start off aggressive and gradually become more conservative as you approach retirement.

In short: one fund, one decision, long-term plan.

A Brief History

Target date funds emerged in the early 1990s, but they really took off after the Pension Protection Act of 2006. This law allowed employers to automatically enroll employees into 401(k) plans and use target date funds as the default investment option.

That move changed everything. Suddenly, millions of Americans were investing—many for the first time—and target date funds became the go-to solution for people who wanted a smart, hands-off approach to retirement planning.

The Glide Path: Built-in Risk Adjustment

Every target date fund follows a glide path—a formula that shifts your asset allocation over time. Early in your career, the fund leans heavily into stocks to capture growth. As retirement nears, it moves gradually into bonds and other lower-risk assets to protect your savings.

This transition is designed to reflect how your ability to take risk changes over time. When you’re younger, you can afford to ride out market dips. But later in life, preserving what you’ve saved becomes more important than chasing high returns.

The Skiing Analogy: Rails on Edge

Think of investing like skiing. When you’re young and full of energy, you carve hard turns with your rails on edge, moving fast and taking on steep slopes. If you fall, you likely bounce back.

But as you age, your definition of “rails on edge” shifts. A high-speed crash in your 20s might mean a bruise. In your 60s, it could mean months of rehab. So you start skiing smarter—less risk, more control.

Target date funds follow that same principle: take appropriate risk while you’re young and build wealth, then gradually shift toward safety and stability as you near retirement. It’s not about fear—it’s about making sure one bad turn doesn’t undo decades of progress.

Dollar Cost Averaging and Volatility

Most people invest in target date funds through regular contributions to a 401(k). This takes advantage of dollar cost averaging—buying into the market at consistent intervals, regardless of price.

In the accumulation phase, this works in your favor. Volatility means you sometimes buy more shares when prices are low, boosting long-term returns. But in retirement, that same volatility can work against you. You’re no longer buying—you’re withdrawing—and downturns can shrink your portfolio just when you need it most. That’s why target date funds taper off risk as you get older.

Why They Dominate 401(k)s

Target date funds are now the default investment in most 401(k) plans—and for good reason:

- Automatic asset allocation

- Diversified holdings

- Risk adjustment over time

- No need to rebalance manually

- Alignment with retirement goals

They’re ideal for investors who want a long-term plan without the hassle of managing it.

One Size Doesn’t Always Fit All in Retirement

While target date funds are excellent during your working years, they may not provide the customization you need once you retire. Retirement often brings new priorities: income planning, tax strategy, healthcare expenses, and legacy goals.

At that stage, a more personalized approach may be necessary.

One way to get that is by working with a competent financial advisor—someone who can help tailor your portfolio to your specific needs and guide you through the complexities of life after work.