One of the fastest ways to learn something new is by mapping it onto something you already understand. That’s how I teach—and how I learn. I take a familiar framework and overlay it onto the new concept I’m trying to grasp.

This post is about asset allocation. Fancy term, simple idea: how much of your money should go into stocks and how much into bonds?

If you’ve read my earlier post about ETFs vs. Mutual Funds, you already know I prefer ETFs for both stocks and bonds. Many advisors will throw around terms like “equities” and “fixed income,” but I try to keep things grounded in everyday language. Not everyone loves the markets or has a background in finance, so my goal is to make the complex feel simple.

That’s also why my daughter once asked me for a book about money—and I didn’t have a ready answer. I’m writing that book now. This post will likely find a home in it.

Let’s get into the analogy.

Maine vs. Montana: A Portfolio Personality Test

I live in two states:

-

- Maine = Slow down, relax, take it easy.

- Montana (Bozeman and surrounding) = Risk-on, rock and roll, YOLO.

That’s stocks and bonds in a nutshell.

-

- Stocks are Montana. They move fast. They’re wild. You can build wealth quickly, but you’re also exposed to big swings. Up 30%, down 25%, back up 40%—it’s a ride.

- Bonds are Maine. Slower. Calmer. More predictable.

If you want to reach your long-term financial goals, combining stocks and bonds can be a smart approach. How much of each depends on two key things: your age and your risk tolerance.

Age, Risk, and Corbett’s Couloir

In general, the older you get, the less risk you want to take. That’s normal—and smart. If you mess up financially in your 60s, you don’t have decades to recover like you did at 23. Same goes for your body. When I was younger, I skied Corbett’s Couloir in Jackson Hole. I wouldn’t do it now. Not because I couldn’t—because I shouldn’t.

Investing’s no different. As you age, you trade speed for safety.

Let’s bring in another analogy.

The Tortoise and the Hare

We all know the story. Slow and steady wins the race. But here’s the thing: you need both. A good portfolio has rabbits and turtles.

-

-

- Stocks = Rabbits: They leap. They sprint. They sometimes face plant.

- Bonds = Turtles: They plod. They don’t panic. They keep going.

-

Let’s say you’re hiking a 14er (a mountain over 14,000 feet). You’re not racing anyone. The goal is to reach the summit without burning out or breaking down. Same with investing.

Sample Portfolios: Matching the Mix to the Mission

Below are three example portfolios. Each is suited for a different life stage and risk tolerance.

70% Stocks / 30% Bonds

- Who it’s for: Younger investors or those with a high risk tolerance.

- What to expect: Volatility. This portfolio could drop from $100,000 to $70,000 and back to $120,000 within three years.

- Real-world example: Think COVID. The market tanked, then hit new highs faster than most expected.

- Key question: If your portfolio dropped 30%, would you panic and sell? If yes, this allocation isn’t for you.

60% Stocks / 40% Bonds

- Who it’s for: Middle-aged investors or those with a moderate risk tolerance.

- Behavior: Stocks still drive growth, but the bond allocation softens the blow of downturns.

- Back to the analogy: The rabbit still runs, but the turtle keeps it from darting off a cliff.

50% Stocks / 50% Bonds

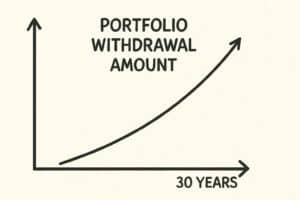

- Who it’s for: Older investors or anyone withdrawing more than 5% annually from their portfolio.

- Why it works: More balance. Less exposure to big market swings.

- Important concept: Withdrawal rate—how much you’re taking out annually. If you withdraw $25,000 from a $500,000 portfolio, that’s a 5% withdrawal rate. I’ll cover this in detail in another post, but it’s a critical piece of retirement planning.

The Takeaway

Asset allocation is about finding the right mix of growth and safety to match your goals, age, and temperament. Some people can figure this out on their own. Others need help from a financial advisor. Either is fine.

Think of it like car repair.

- If you’re comfortable under the hood, go for it.

- If not, go to a mechanic you trust.

Finance is the same. You don’t have to be an expert—you just need to know what kind of trip you’re on, what gear you need, and how fast you want to go.

And whether your vibe is Maine or Montana, rabbit or turtle, there’s a portfolio that fits.