You might’ve thought I wasn’t coming back. That’s fair — a lot of people start talking about financial planning and then disappear when it gets messy. But that’s what I do. I help clients walk straight into their messy financial lives and make sense of it all.

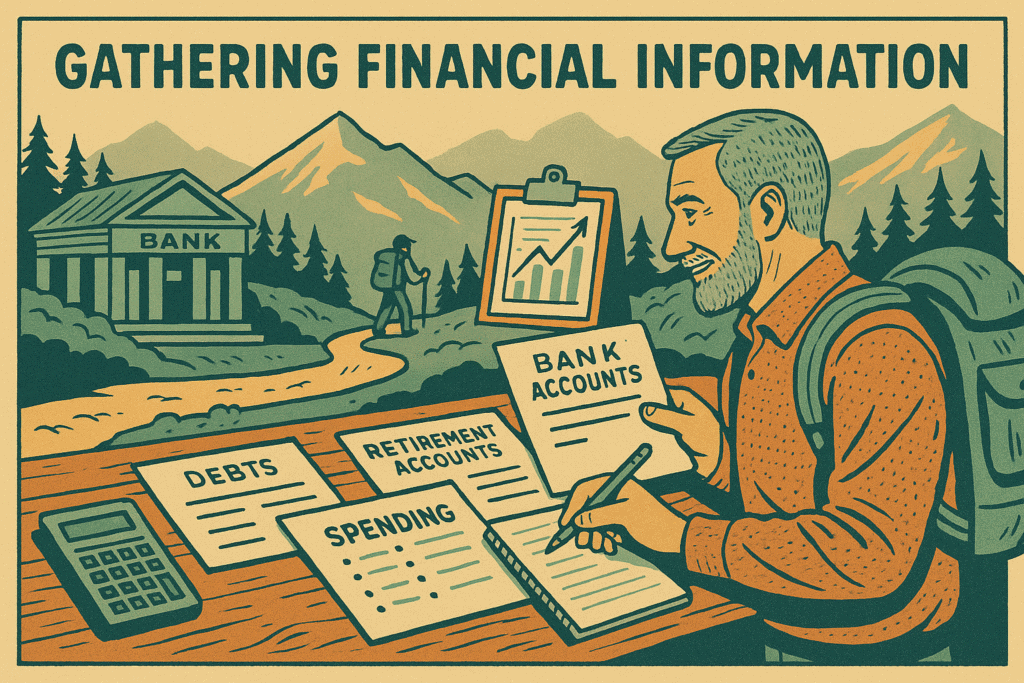

So let’s start with the first step in building a real plan: gathering the data. No fluff, no theory — just what you actually need to know and track.

If you happened to miss the first part of this series – you read it 👉 here.

Bank Assets

Start with your most basic financial tools: checking and savings accounts.

What you need to know:

- How much is in each account

- Where the account is held (Bank, Credit Union, etc.)

- How the account is titled — individually, jointly, in a trust, etc.

If you have assets titled in your children’s names for estate planning reasons — that’s a whole other conversation (and maybe one worth revisiting).

Non-Retirement Assets (aka Brokerage Accounts)

These accounts often come with confusing names. You might hear them referred to as brokerage account or taxable accounts. Regardless, the information is the same as you need for your bank accounts.

What you need to know:

- Account balances

- How they’re titled (individual, joint, trust, etc.)

- What investments are held inside (funds, stocks, bonds, etc.)

- How much you contribute each year or month

Retirement (Tax-Deferred) Accounts

These include any account where the taxes are deferred until withdrawal:

- 401(k)

- 403(b)

- 457 plans

- Traditional IRA

- Roth IRA

- SEP or SIMPLE IRAs

What you need to know:

- Current balance

- Contribution rate (percentage or dollar amount)

- Employer match, if any

- Investments held

Debts

You can’t make a solid plan without accounting for your obligations. List every debt:

- Mortgage

- Car loans

- Credit cards

- Student loans

- Personal loans

What you need to know:

- Outstanding balance

- Monthly payment

- Interest rate

- Original date and term of the loan

This information helps you (or me) amortize the debt — meaning we can model how it’ll be paid down over time.

Current Spending Habits

Before you can build a realistic budget, you need to know what you’re actually spending right now. This is part of the data-gathering phase — and often the biggest shock for people: “We spend how much on what?”

It’s like trying to get fit: the first step is stepping on the scale.

What I need to know:

- Total spending by category (e.g., groceries, dining, subscriptions, etc.)

- Recurring expenses vs. one-time purchases

- Where the money is going — not where you think it’s going

How to get it:

- Export your last 3–6 months of transactions from your bank and credit card accounts

- Use Excel or Google Sheets to sort, filter, and categorize

- Be honest — this isn’t about judgment, it’s about clarity

This raw spending data becomes the foundation for your budget, your cash flow plan, and ultimately, your financial decisions.

Real Assets

Most people start here because these are their biggest-ticket items — but that’s not always helpful.

People love to say: “I’ve got $500,000 in home equity.” Great — but what does that actually mean?

Here’s the question: Do you plan to move to a lower-cost area in retirement?

- If yes — awesome. That equity could be part of your retirement strategy.

- If no — and you’re staying put — then that equity isn’t usable. You have to live somewhere.

Unless you’re downsizing or relocating, your home equity isn’t really a liquid asset. So stop treating it like it’s part of your retirement cash.

Coming Up Next

Once you’ve gathered this data, you’ll use it to build your:

- Net Worth Statement

- Cash Flow Statement

- Spending Plan

These are the cornerstones of your plan. Next post, I’ll show you exactly how to structure them.