Now that you’ve built your Net Worth Statement, Cash Flow Statement, and Spending Plan, it’s time to tackle your first major goal: retirement.

Why Start With Retirement First?

Because after buying a home, it’s the next fundamental human need — shelter, then security.

And nothing defines long-term security like knowing you can afford to stop working someday.

The three slides below show why:

Slide 1 – The Youth Stage

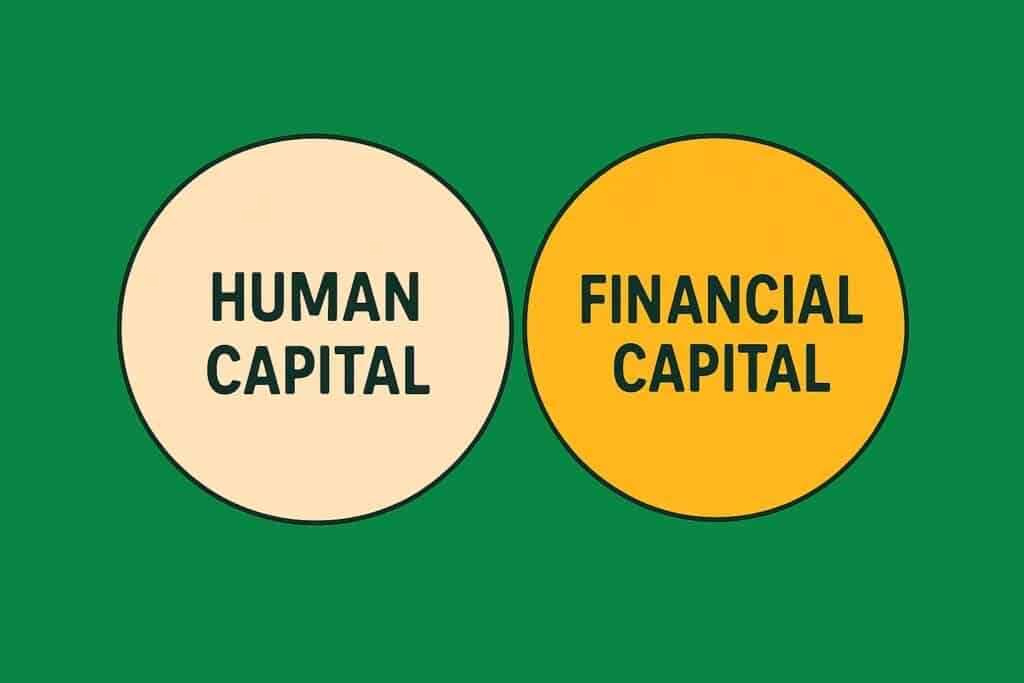

In your twenties, most of your wealth lives inside you. You have human capital — energy, creativity, time, and the ability to work hard for decades ahead. You have a lot of human potential.

But you probably don’t have much financial capital yet. That’s normal. You’re trading time for money, building skills, and laying the foundation for future growth.

Slide 2 – The Builder Stage

As you move through life, the balance begins to shift. Your human capital gradually converts into financial capital — if you save and invest along the way.

How quickly this happens depends on two levers:

- Increase your income – grow your skills, take risks, build businesses, or advance your career.

- Reduce your expenses – live intentionally and keep margin in your life. Together, these levers form your Spending Plan — the bridge between effort and freedom.

Slide 3 – The Retirement Years

Eventually, your human capital fades. You have less time, energy, and capacity to work. This is when your financial capital must take over — supporting you, protecting you, even paying others to help with what you once did yourself.

Growing older is hard; growing older without enough financial capital is much harder. The time to prepare is now — while your human capital is still abundant.

Ignoring that reality is dangerous. Pretending you’ll never get old isn’t optimism — it’s denial. Better to plan while you can still build momentum.

Moving From Human Capital to Financial Capital

The simplest, most powerful way to shift capital from the left circle to the right is through automatic, periodic investing — money that leaves your paycheck before you even see it.

That means using your employer’s plan: 401(k), 403(b), 457, SIMPLE IRA, SEP, or another qualified plan.

If you’re self-employed, I wrote a separate post about choosing the right retirement plan. But the real magic is in setting up auto-pilot contributions — the same amount, every month, no matter what.

If you have a bookkeeper or CPA, they can help automate it. Payroll companies can too.

And if you’re a solo-preneur? Link your operating account directly to your retirement account and set recurring transfers. Most investment firms make this easy — just be sure the one you choose does.

This steady rhythm of investing is called Dollar Cost Averaging. It’s how you build wealth quietly and consistently — even while you sleep.

Step 1: Estimate Your Retirement Spending

Before we calculate what you’ll need saved, start by estimating how much you’ll spend.

A quick rule of thumb: Begin with 80% of your current total spending — without taxes. We’re trying to isolate your spending lifestyle, not your gross income.

EXAMPLE

Fixed Expenses

$60,0000

Variable Expenses

$40,000

Current Spending Plan

$100,000

For illustrational purposes only. Your numbers will of course be different.

Now, multiply your current spending plan by 80%:

$100,000 × 0.8 = $80,000 – The Retirement Spending Goal

Is it perfect? Of course not. But it’s a solid first draft. We’ll refine it later — for now, it’s about direction, not perfection.

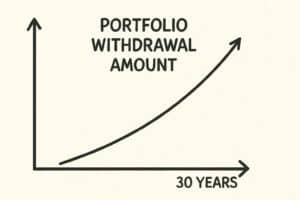

Step 2: Back Into Your Portfolio Target

Here’s the basic math:

Portfolio Withdrawal Amount

Retirement Spending Goal

$80,000

Retirement Income Sources

-$30,000

Portfolio Withdrawal Amount

$50,000

For illustrational purposes only. Your numbers will of course be different.

What are your retirement income sources; Social Security (get your estimate at here), pensions, net income from rental properties. Any income you expect to continue after you stop working.

WHAT ABOUT WITHDRAWAL RATES?

If you’re retiring around age 67, use a 4.5% withdrawal rate as a safe starting point.

To calculate how large of a portfolio you’ll need. Move the decimal two places to the left on the 4.5%:

$50,000 ÷ 0.045 = $1,111,111

That’s your approximate target portfolio at retirement.

Big number? Maybe. But with time and consistency, it’s absolutely achievable.

That figure in today’s dollars. You still have to convert this sum into future dollars. I’ll teach you how in my next post – Look Ahead: Forecast Your Future.

Step 3: Focus on Systems, Not Math

You don’t need advanced formulas. Everything here uses math you learned by sixth grade.

What really matters is discipline and automation — the compounding effect of steady contributions and the passage of time.

The longer you wait, the steeper the climb. I know — I started late.

In 2009, my net worth was –$135,000. That was negative if you didn’t catch it. I was in debt. I owed more than I owned and I was 40 years old, with two kids still to put through college.

I woke up one day – scared. I was losing sleep due to financial stress.

Why would a financial advisor share that? Because if you’re in that spot now — you can still climb out. I did.

It was a steep climb in the early going. For you hikers, that means no switchbacks.

How did I turn it around? My Financial Planning Made Simple series can teach you how.

Read it. Study it. Implement it.

Set up your own “set it and forget it” strategies. They just might work for you too.

Step 4: Track Your Climb

I’ve kept a Net Worth spreadsheet in Google Sheets since 2009.

- At the top: the date.

- Below: the line items from the Net Worth Statement you built in Filling Out Your Net Worth Statement.

It was no fun at first but I had to get on the scale. I had to know where I was starting from.

In order to make life changes – you first have to admit where you’re at.

Just like a scale, I updated (weighed) my spreadsheet periodically. It was my way of staying accountable. In the early years, I updated it quarterly — I was obsessed with the climb.

Now? Once a year. Because it’s on auto-pilot.

That’s the goal: build a plan you can set, trust, and let time do its work.

In Closing

Retirement planning isn’t about fancy math — it’s about momentum. Build the foundation first, just like a house built for Maine and Montana winters. You can choose the countertops later.

Get the basics right — automate, track, and keep climbing — and you’ll discover the quiet power of compounding.

Because when your plan is on auto-pilot, you’re already halfway there.

Still have questions about determining your Retirement Spending Goal? 🤔💰🧾

Check out the Financial Planning Made Easy FAQ’s for clear answers and practical tips that’ll keep you moving forward.