I have clients earning $250K, $300K, or more ask about Roth IRAs or converting to one, they usually come in with strong opinions—often shaped by internet advice that doesn’t apply to their financial reality.

The Roth IRA has a certain appeal: tax-free growth, no RMDs during the owner’s lifetime, and a potentially favorable legacy benefit. But that appeal often fades when you look at the numbers—especially for high earners under the current tax code.

Let’s cut to the chase: your current tax bracket matters—a lot. And so does your age, your retirement timeline, and the structure of your assets.

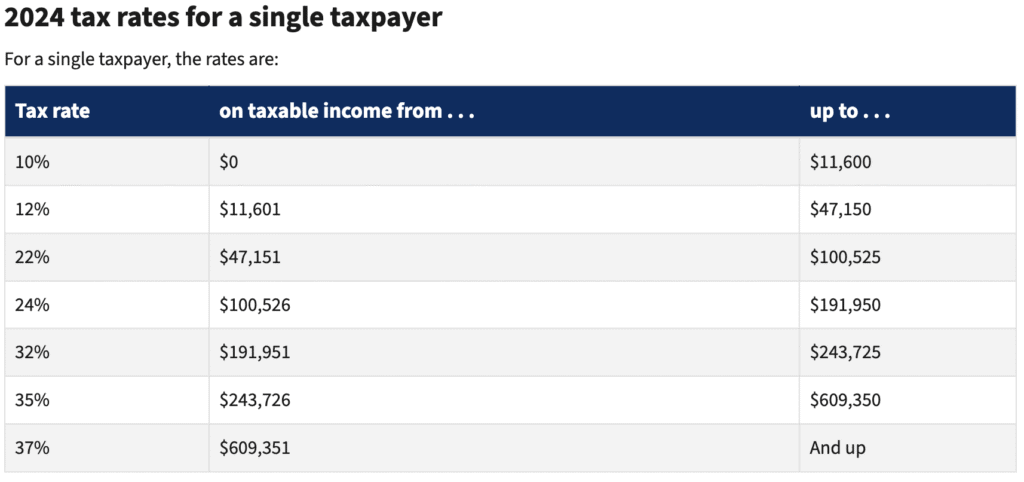

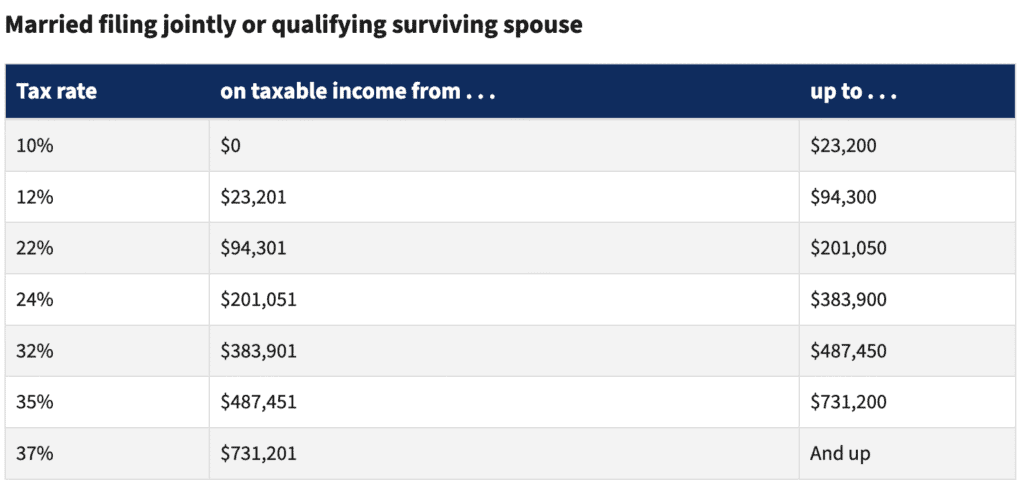

Below are the single and married filing jointly tax tables for 2024.

Traditional IRA: A Bird in the Hand

If you’re earning $400K+ a year, you’re likely in the 32%, 35%, or even 37% federal tax bracket. A traditional IRA or pre-tax 401(k) gives you a tax break now, when it actually counts. You reduce taxable income today, lower your effective tax rate, and free up more capital to invest or save elsewhere.

That tax deduction isn’t just a short-term win. If you retire with a more moderate lifestyle, your income—and tax rate—could be much lower later. For most high earners, even with healthy retirement savings, future withdrawals are unlikely to be taxed at today’s top marginal rates, unless they also hold significant taxable investments or deferred income streams.

In other words: you’re taking a 37% deduction now to pay 22% or 24% later. That’s a win.

Roth IRA: Long-Term Play with Short-Term Pain

Roth IRAs and Roth 401(k)s are attractive because the distributions are tax-free in retirement. That’s a great deal—if you’re in a low or moderate tax bracket now and expect to be in a higher bracket later.

But that’s rarely the case for high-income earners, especially in their 40s, 50s, or 60s. For a 55-year-old making $325K, the math on a Roth conversion is painful. You’re essentially volunteering to pay taxes at today’s highest rates to avoid potentially lower rates later. That tradeoff often doesn’t pencil out unless:

- You have no need for the money and plan to leave it as a legacy.

- You have many years (15–20+) for the tax-free growth to compound.

- You strongly believe taxes will rise significantly in retirement (and they might, but we don’t plan with crystal balls).

Age and Time Horizon Matter

For younger high earners in their early 30s, who haven’t hit peak income yet and have decades before retirement, Roth contributions may make more sense—especially if they’re in a temporarily lower tax bracket due to business losses, sabbaticals, or career shifts.

But for clients in their late 40s or older, who are already in a high bracket, the traditional path often makes more sense. The older you are, the less time your Roth dollars have to grow, and the more the upfront tax hit hurts.

A Note on Roth Conversions

Roth conversions are often pitched as a smart move before RMD age. And in some cases, they are—especially in the gap years between retirement and RMDs (usually from 60–72). If you retire early and have a few low-income years before Social Security or RMDs kick in, that’s the sweet spot. You can convert at 12% or 22% and reduce future RMDs. But that’s very different from converting while still earning $300K+.

The Bottom Line

The Roth IRA is not a one-size-fits-all solution. For high-income earners, especially those over 45, the traditional IRA or 401(k) often provides a clearer path to tax efficiency and retirement income planning. Deferring the tax bill until later—when your income is likely lower—can lead to better overall outcomes.

Yes, Roths are powerful. But they’re not always the smart move.

As always: the right answer depends on your situation. But in most high-income scenarios, taking the deduction now and planning smartly for later wins.