Now that you’ve gathered all your financial information, it’s time to pull it together into a clear, actionable plan. Think of this like starting a fitness program.

When you visit your doctor, they take your vitals—weight, BMI, blood pressure, maybe some labs—so you know your baseline before creating a health plan.

Financial planning works the same way: you need to know where you stand before you can move forward.

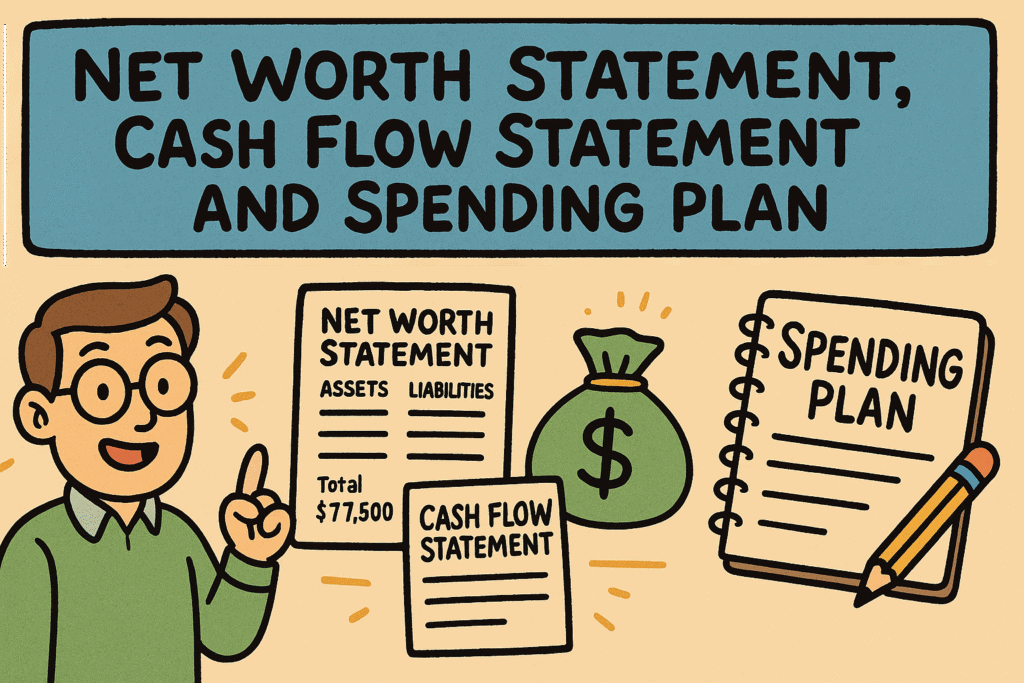

There are three key tools we’ll focus on:

Net Worth Statement

Also known as a balance sheet or statement of financial position. I prefer the term Net Worth Statement—it’s clearer and more empowering. This document gives you a snapshot of what you own vs. what you owe. It’s your financial baseline.

Cash Flow Statement

This shows where your money is going. Some call it an income and expense report, but I stick with Cash Flow Statement because it emphasizes movement—how money flows through your life. Unless you were born into wealth or expect a major inheritance (which I tell clients not to count on), your income is your most powerful wealth-building tool. Knowing where it’s going is the first step toward using it more effectively.

Spending Plan

You might know this as a budget, but I prefer Spending Plan. Why? Because it suggests control, choice, and intention—not restriction. It’s not about saying “no,” it’s about deciding what to say “yes” to.

📎 Download the templates I use with my family and clients:

Let’s start with the Net Worth Statement. Print out the template so you can follow along as I walk you through how to complete it.

Where to Find the Cash Flow Template

There are three tabs in the spreadsheet. The first tab is the Net Worth Statement.

Filling Out Your Net Worth Statement

It’s divided into two columns: Assets (on the left) and Liabilities (on the right).

Assets

We break this into three sections:

Cash & Cash Equivalents –These are liquid assets—things you can easily convert to cash.

Examples:

- Checking accounts

- Savings accounts

- Money market funds

- Short-term CDs

- Treasury bills

(Skip physical items or stocks/bonds here—they belong in other sections. If you hold long-term CDs, you can create a separate section for those.)

Investment Assets

- Non-retirement accounts: brokerage, individual, joint, trust (if applicable).

Use initials to indicate ownership (e.g., JT for joint). - Retirement accounts: IRAs, Roth IRAs, 401(k), 403(b), 457, etc.

If you can’t access the money without penalty before age 59½, it goes here.

Include inherited IRAs too.

Personal Use Assets: These are things you own but probably won’t use to fund your retirement.

Examples:

- Your home

- Vehicles

- Jewelry

- Art or collectibles

If you have assets you do plan to liquidate for future goals (like a second home or a valuable collection), create an additional section called Illiquid Investments. This might include:

- Rental properties

- Business interests

- Collectibles

Each section has formulas at the bottom to calculate subtotals. Total all asset categories together to get your Total Assets.

Liabilities

On the right side, list all your current debts. Just include the balance—no need for interest rates, payment amounts, or due dates here.

Examples:

- Mortgage

- Car loans

- Student loans

- Credit card debt

- Personal loans

At the bottom, total all your debts. That gives you your Total Liabilities.

Calculating Net Worth

At the bottom of the template, subtract Total Liabilities from Total Assets. That number is your Net Worth.

This is your starting point. It may not be where you want to be yet, but it’s where you are—and that’s powerful. You can’t build financial momentum until you know where you stand.

Next up: we’ll break down how to build your Cash Flow Statement, then move on to your Spending Plan.

Still have questions about creating your Net Worth Statement? 🤔💰🧾

Check out the Financial Planning Made Easy FAQ’s for clear answers and practical tips that’ll keep you moving forward.